Stamford, CT -

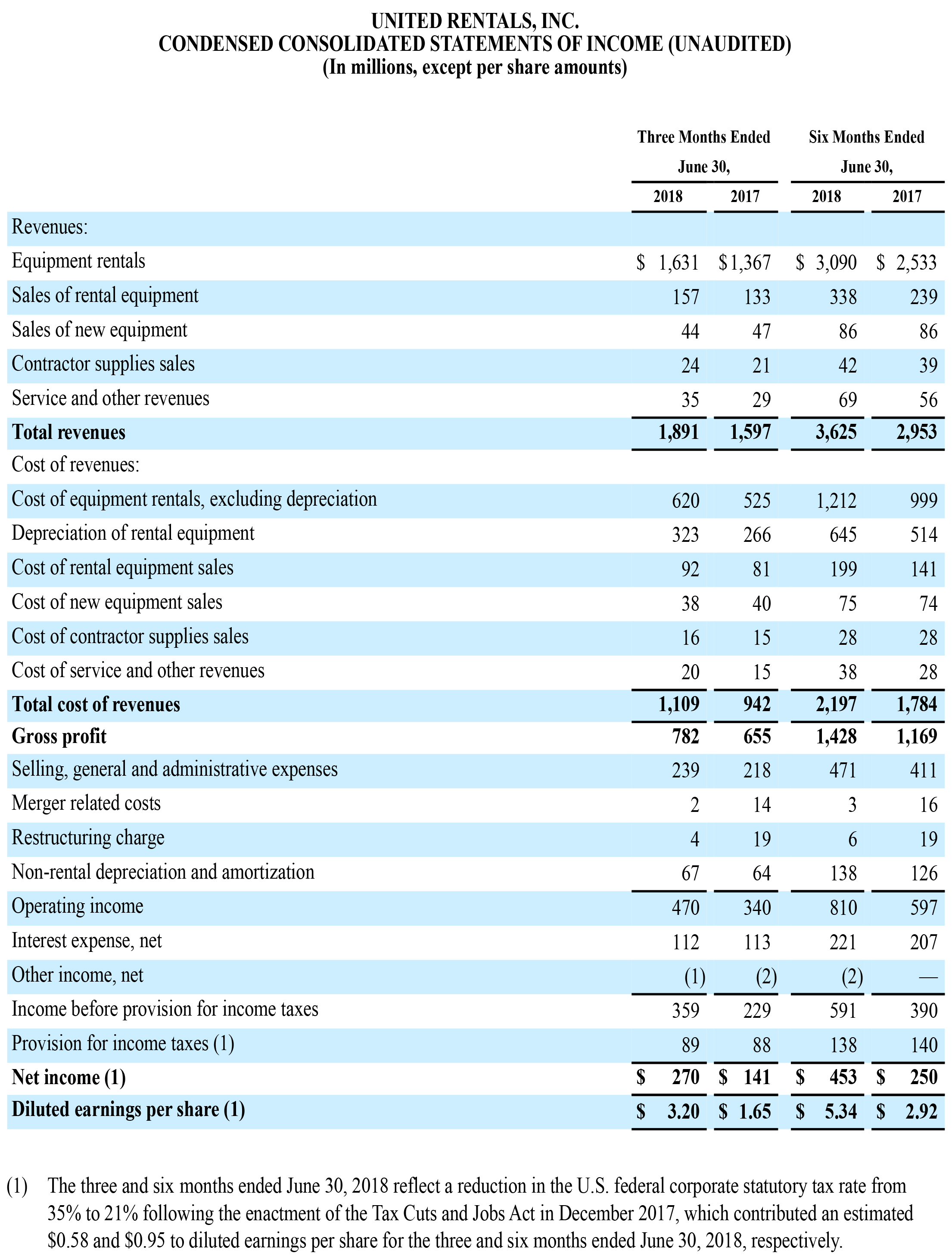

United Rentals, Inc. (NYSE: URI) today announced financial results for the second quarter 20181. Total revenue was $1.891 billion and rental revenue was $1.631 billion for the second quarter, compared with $1.597 billion and $1.367 billion, respectively, for the same period last year. On a GAAP basis, the company reported second quarter net income of $270 million, or $3.20 per diluted share, compared with $141 million, or $1.65 per diluted share, for the same period last year. The second quarter 2018 includes a net income benefit associated with the Tax Cuts and Jobs Act (the “Tax Act”) that was enacted in December 2017. The Tax Act reduced the U.S. federal corporate statutory tax rate from 35% to 21%, which contributed an estimated $0.58 to earnings per diluted share for the second quarter 20182.

Adjusted EPS3 for the quarter was $3.85 per diluted share, compared with $2.37 per diluted share for the same period last year. The reduction in the tax rate discussed above contributed an estimated $0.70 to adjusted EPS for the second quarter 20182. Adjusted EBITDA3 was $907 million and adjusted EBITDA margin3 was 48.0%, reflecting increases of $160 million and 120 basis points, respectively, from the same period last year.

Second Quarter 2018 Highlights

- Rental revenue4 increased 19.3% year-over-year. Within rental revenue, owned equipment rental revenue increased 19.3%, reflecting increases of 15.9% in the volume of equipment on rent and 2.8% in rental rates.

- Pro forma1 rental revenue increased 11.4% year-over-year, reflecting growth of 7.1% in the volume of equipment on rent and a 2.8% increase in rental rates.

- Time utilization decreased 20 basis points year-over-year to 69.2%, primarily reflecting the impact of the Neff acquisition. On a pro forma basis, time utilization was flat year-over-year.

- The company’s Trench, Power and Pump specialty segment's rental revenue increased by 33.5% year-over-year, including a 21.9% increase on a same store basis. The segment’s rental gross margin decreased by 110 basis points to 48.5%.

_______________

1. The company completed the acquisitions of NES Rentals Holdings II, Inc. (“NES”) and Neff Corporation ("Neff") in April 2017 and

October 2017, respectively. NES and Neff are included in the company's results subsequent to the acquisition dates. Pro forma results

reflect the combination of United Rentals, NES and Neff for all periods presented.

2. The estimated contribution of the Tax Act was calculated by applying the percentage point tax rate reduction to U.S. pretax income and

the pretax adjustments reflected in adjusted EPS.

3. Adjusted EPS (earnings per share) and adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) are non-

GAAP measures that exclude the impact of the items noted in the tables below. See the tables below for amounts and reconciliations

to the most comparable GAAP measures. Adjusted EBITDA margin represents adjusted EBITDA divided by total revenue.

4. Rental revenue includes owned equipment rental revenue, re-rent revenue and ancillary revenue.

- The company generated $157 million of proceeds from used equipment sales at a GAAP gross margin of 41.4% and an adjusted gross margin of 51.6%, compared with $133 million at a GAAP gross margin of 39.1% and an adjusted gross margin of 52.6% for the same period last year. The year-over-year increase in used equipment sales primarily reflects increased volume, driven by a significantly larger fleet size, in a strong used equipment market.5

BakerCorp Acquisition

On 2 de julio de 2018, the company announced that it has entered into a definitive agreement to acquire BakerCorp International Holdings, Inc. (“BakerCorp”) for approximately $715 million in cash. BakerCorp is a leading provider of rental solutions for fluid storage, transfer and treatment, with approximately $295 million in annual revenue and 950 employees. BakerCorp’s operations are primarily concentrated in the United States and Canada, where it has 46 locations, with another 11 locations in France, Germany, the United Kingdom and the Netherlands. The transaction is expected to close early in the third quarter and contribute approximately $140 million of revenue and $40 million of adjusted EBITDA to full-year 2018 results, while adding approximately $50 million to the 2018 capital spending plan.

CEO Comments

Michael Kneeland, chief executive officer of United Rentals, said, "We were very pleased with the momentum of our business in the second quarter, as strong gains in volume and rates helped drive better than 11% growth in pro forma rental revenue. Importantly, demand remained robust across our construction and industrial verticals in both the U.S. and Canada. The Neff integration is largely complete, and we look forward to getting the process started with Baker this quarter." Kneeland continued, "Everything we see internally and externally points to a durable cycle and continued industry discipline in managing fleet growth. Given this backdrop, we’ve raised our 2018 guidance for total revenue, adjusted EBITDA and capex. We remain focused on executing a balanced strategy of growth and returns to maximize long-term value."

Six Months 2018 Highlights

- Rental revenue increased 22.0% year-over-year. Within rental revenue, owned equipment rental revenue increased 22.1%, reflecting increases of 20.6% in the volume of equipment on rent and 2.4% in rental rates.

- Pro forma rental revenue increased 10.7% year-over-year, reflecting growth of 7.0% in the volume of equipment on rent and a 2.8% increase in rental rates.

- Time utilization decreased 60 basis points year-over-year to 67.2%, primarily reflecting the impact of the NES and Neff acquisitions. On a pro forma basis, time utilization decreased 10 basis points year-over-year.

- The company’s Trench, Power and Pump specialty segment's rental revenue increased by 34.9% year-over-year, including a 23.7% increase on a same store basis. The segment’s rental gross margin increased by 20 basis points to 47.4%.

- The company generated $338 million of proceeds from used equipment sales at a GAAP gross margin of 41.1% and an adjusted gross margin of 53.0%, compared with $239 million at a GAAP gross margin of 41.0% and an adjusted gross margin of 51.9% for the same period last year. The year-over-year increase in used equipment sales primarily reflects increased volume, driven by a significantly larger fleet size, in a strong used equipment market.5

_______________

5. Used equipment sales adjusted gross margin excludes the impact of the fair value mark-up of acquired RSC, NES and Neff fleet that was sold. In 2018, we adopted Accounting Standards Codification (“ASC”) Topic 606, “Revenue from Contracts with Customers”. Used equipment sales in the second quarter of 2017 would have been reduced by $12 under Topic 606 because such sales would have been recognized prior to the second quarter. Under Topic 606, we would have recognized an additional $12 of sales of rental equipment during the first six months of 2017. While the adoption of Topic 606 impacted the timing of revenue recognition, it has no impact on annual revenue.

2018 Outlook

The following revised full-year guidance does not include the impact of the pending acquisition of BakerCorp. For additional detail on BakerCorp, please see the section above, as well as the investor presentations that are currently accessible on www.unitedrentals.com.

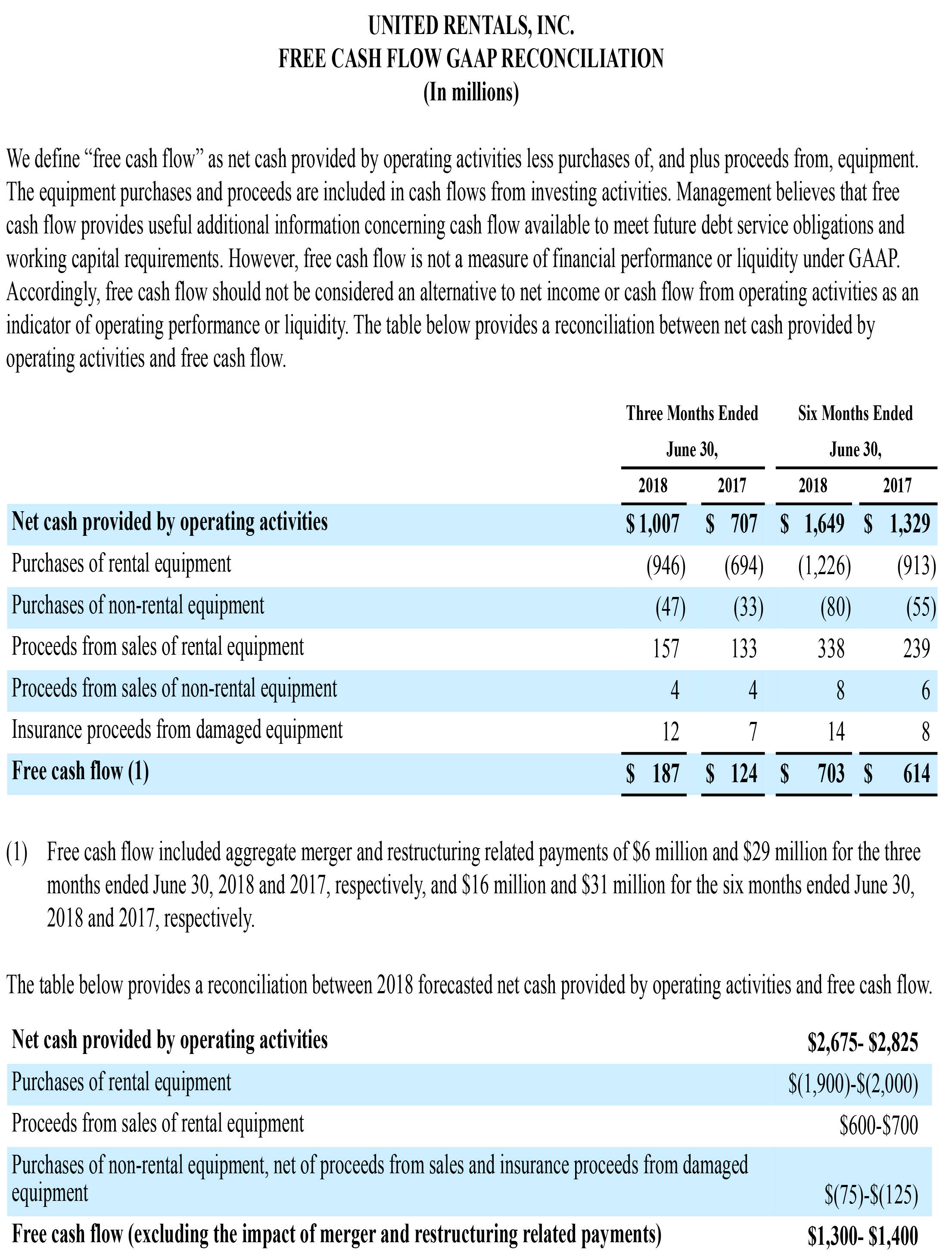

Free Cash Flow and Fleet Size

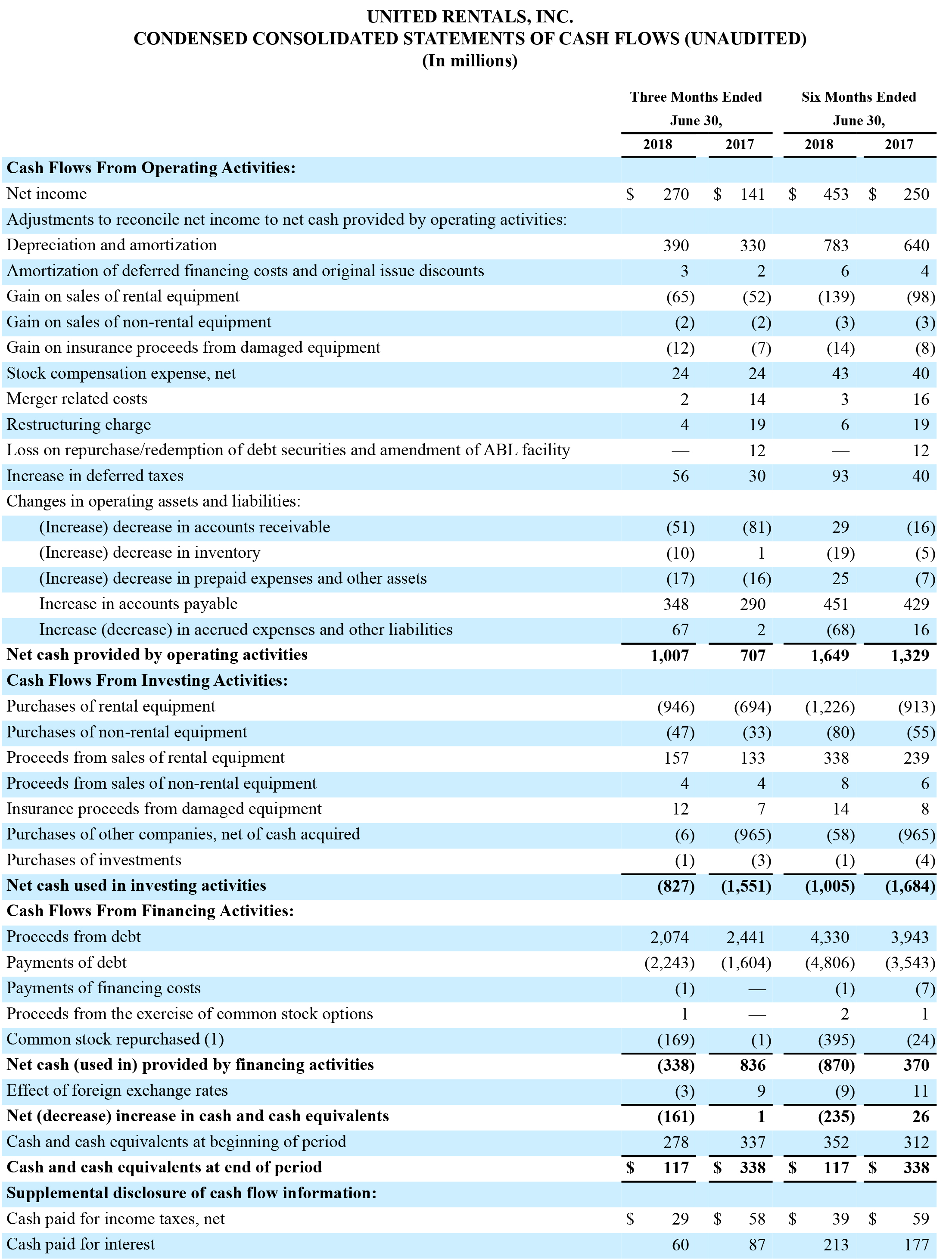

For the first six months of 2018, net cash provided by operating activities was $1.649 billion, and free cash flow was $703 million after total rental and non-rental gross capital expenditures of $1.306 billion. For the first six months of 2017, net cash provided by operating activities was $1.329 billion, and free cash flow was $614 million after total rental and non-rental gross capital expenditures of $968 million. Free cash flow for the first six months of 2018 and 2017 included aggregate merger and restructuring related payments of $16 million and $31 million, respectively.

The size of the rental fleet was $11.98 billion of OEC at 30 de junio de 2018, compared with $11.51 billion at 31 de diciembre de 2017. The age of the rental fleet was 46.0 months on an OEC-weighted basis at 30 de junio de 2018, compared with 47.0 months at 31 de diciembre de 2017.

Return on Invested Capital (ROIC)

ROIC was 10.0% for the 12 months ended 30 de junio de 2018, compared with 8.4% for the 12 months ended 30 de junio de 2017. The company’s ROIC metric uses after-tax operating income for the trailing 12 months divided by average stockholders’ equity, debt and deferred taxes, net of average cash. To mitigate the volatility related to fluctuations in the company’s tax rate from period to period, the U.S. federal corporate statutory tax rates of 21% and 35% for 2018 and 2017, respectively, were used to calculate after-tax operating income.

The company expects ROIC to materially increase due to the reduced tax rates following the enactment of the Tax Act, but, because the trailing 12 months are used for the ROIC calculation, the full impact will not be reflected until one year after the lower tax rate became effective. If the 21% U.S. federal corporate statutory tax rate following the enactment of the Tax Act was applied to ROIC for all historic periods, the company estimates that ROIC would have been 10.9% and 10.0% for the 12 months ended 30 de junio de 2018 and 2017, respectively.

Share Repurchase Program

The company completed its $1 billion program to repurchase shares of its common stock in the second quarter 2018. Following its completion, in July 2018, the company commenced a new $1.25 billion share repurchase program, which the company intends to complete by the end of 2019.

_______________

6. Information reconciling forward-looking adjusted EBITDA to the comparable GAAP financial measures is unavailable to the company without unreasonable effort, as discussed below.

7. Free cash flow is a non-GAAP measure. See the table below for amounts and a reconciliation to the most comparable GAAP measure.

Conference Call

United Rentals will hold a conference call tomorrow, jueves, julio 19, 2018, at 11:00 a.m. Eastern Time. The conference call number is 855-458-4217 (international: 574-990-3618). The conference call will also be available live by audio webcast at unitedrentals.com, where it will be archived until the next earnings call. The replay number for the call is 404-537-3406, passcode is 2978447.

Non-GAAP Measures

Free cash flow, earnings before interest, taxes, depreciation and amortization (EBITDA), adjusted EBITDA, and adjusted earnings per share (adjusted EPS) are non-GAAP financial measures as defined under the rules of the SEC. Free cash flow represents net cash provided by operating activities less purchases of, and plus proceeds from, equipment. The equipment purchases and proceeds represent cash flows from investing activities. EBITDA represents the sum of net income, provision for income taxes, interest expense, net, depreciation of rental equipment and non-rental depreciation and amortization. Adjusted EBITDA represents EBITDA plus the sum of the merger related costs, restructuring charge, stock compensation expense, net, and the impact of the fair value mark-up of acquired fleet. Adjusted EPS represents EPS plus the sum of the merger related costs, restructuring charge, the impact on depreciation related to acquired fleet and property and equipment, the impact of the fair value mark-up of acquired fleet, the loss on repurchase/redemption of debt securities and amendment of ABL facility, and merger related intangible asset amortization. The company believes that:

(i) free cash flow provides useful additional information concerning cash flow available to meet future debt service obligations and working capital requirements; (ii) EBITDA and adjusted EBITDA provide useful information about operating performance and period-over-period growth, and help investors gain an understanding of the factors and trends affecting our ongoing cash earnings, from which capital investments are made and debt is serviced; and (iii) adjusted EPS provides useful information concerning future profitability. However, none of these measures should be considered as alternatives to net income, cash flows from operating activities or earnings per share under GAAP as indicators of operating performance or liquidity.

Information reconciling forward-looking adjusted EBITDA to GAAP financial measures is unavailable to the company without unreasonable effort. The company is not able to provide reconciliations of adjusted EBITDA to GAAP financial measures because certain items required for such reconciliations are outside of the company’s control and/or cannot be reasonably predicted, such as the provision for income taxes.

Preparation of such reconciliations would require a forward-looking balance sheet, statement of income and statement of cash flow, prepared in accordance with GAAP, and such forward-looking financial statements are unavailable to the company without unreasonable effort. The company provides a range for its adjusted EBITDA forecast that it believes will be achieved, however it cannot accurately predict all the components of the adjusted EBITDA calculation. The company provides an adjusted EBITDA forecast because it believes that adjusted EBITDA, when viewed with the company’s results under

GAAP, provides useful information for the reasons noted above. However, adjusted EBITDA is not a measure of financial performance or liquidity under GAAP and, accordingly, should not be considered as an alternative to net income or cash flow from operating activities as an indicator of operating performance or liquidity.

Acerca de United Rentals

United Rentals, Inc. is the largest equipment rental company in the world. The company has an integrated network of 1,008 rental locations in 49 states and every Canadian province. The company’s approximately 15,500 employees serve construction and industrial customers, utilities, municipalities, homeowners and others. The company offers approximately 3,400 classes of equipment for rent with a total original cost of $11.98 billion. United Rentals is a member of the Standard & Poor’s 500 Index, the Barron’s 400 Index and the Russell 3000 Index® and is headquartered in Stamford, Conn. Additional information about United Rentals is available at unitedrentals.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, known as the PSLRA. These statements can generally be identified by the use of forward-looking terminology such as “believe,”“expect,” “may,” “will,” “should,” “seek,” “on-track,” “plan,” “project,” “forecast,” “intend” or “anticipate,” or the negative thereof or comparable terminology, or by discussions of vision, strategy or outlook. These statements are based on current plans, estimates and projections, and, therefore, you should not place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. Factors that could cause actual results to differ materially from those projected include, but are not limited to, the following: (1) the challenges associated with past or future acquisitions, including NES, Neff and BakerCorp, such as undiscovered liabilities, costs, integration issues and/or the inability to achieve the cost and revenue synergies expected; (2) a slowdown in North American construction and industrial activities, which could reduce our revenues and profitability; (3) our significant indebtedness, which requires us to use a substantial portion of our cash flow for debt service and can constrain our flexibility in responding to unanticipated or adverse business conditions; (4) the inability to refinance our indebtedness at terms that are favorable to us, or at all; (5) the incurrence of additional debt, which could exacerbate the risks associated with our current level of indebtedness; (6) noncompliance with covenants in our debt agreements, which could result in termination of our credit facilities and acceleration of outstanding borrowings; (7) restrictive covenants and amount of borrowings permitted under our debt agreements, which could limit our financial and operational flexibility; (8) an overcapacity of fleet in the equipment rental industry; (9) a decrease in levels of infrastructure spending, including lower than expected government funding for construction projects; (10) fluctuations in the price of our common stock and inability to complete stock repurchases in the time frame and/or on the terms anticipated; (11) our rates and time utilization being less than anticipated; (12) our inability to manage credit risk adequately or to collect on contracts with customers; (13) our inability to access the capital that our business or growth plans may require; (14) the incurrence of impairment charges; (15) trends in oil and natural gas could adversely affect demand for our services and products; (16) our dependence on distributions from subsidiaries as a result of our holding company structure and the fact that such distributions could be limited by contractual or legal restrictions; (17) an increase in our loss reserves to address business operations or other claims and any claims that exceed our established levels of reserves; (18) the incurrence of additional costs and expenses (including indemnification obligations) in connection with litigation, regulatory or investigatory matters; (19) the outcome or other potential consequences of litigation and other claims and regulatory matters relating to our business, including certain claims that our insurance may not cover; (20) the effect that certain provisions in our charter and certain debt agreements and our significant indebtedness may have of making more difficult or otherwise discouraging, delaying or deterring a takeover or other change of control of us; (21) management turnover and inability to attract and retain key personnel; (22) our costs being more than anticipated and/or the inability to realize expected savings in the amounts or time frames planned;

(23) our dependence on key suppliers to obtain equipment and other supplies for our business on acceptable terms; (24) our inability to sell our new or used fleet in the amounts, or at the prices, we expect; (25) competition from existing and new competitors; (26) security breaches, cybersecurity attacks and other significant disruptions in our information technology systems; (27) the costs of complying with environmental, safety and foreign laws and regulations, as well as other risks associated with non-U.S. operations, including currency exchange risk; (28) labor difficulties and labor-based legislation affecting our labor relations and operations generally; (29) increases in our maintenance and replacement costs and/or decreases in the residual value of our equipment; and (30) the effect of changes in tax law, such as the effect of the Tax Cuts and Jobs Act that was enacted on 22 de diciembre de 2017. For a more complete description of these and other possible risks and uncertainties, please refer to our Annual Report on Form 10-K for the year ended 31 de diciembre de 2017, as well as to our subsequent filings with the SEC. The forwardlooking statements contained herein speak only as of the date hereof, and we make no commitment to update or publicly release any revisions to forward-looking statements in order to reflect new information or subsequent events, circumstances or changes in expectations.

# # #

Contacto:

Ted Grace

(203) 618-7122

Cel.: (203) 399-8951

tgrace@ur.com

UNITED RENTALS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) (continued)

(1) As discussed above, we have an open $1.25 billion share repurchase program that we intend to complete by the end of

2019. This program commenced in July 2018 following the completion of our $1 billion share repurchase program. para

common stock repurchases include i) shares repurchased pursuant to the $1 billion share repurchase program and ii)

shares withheld to satisfy tax withholding obligations upon the vesting of restricted stock unit awards.